Bobbi Brown, MBA, and Stephen Grossbart, PhD have analyzed the biggest changes in the healthcare industry and 2018 and forecasted the trends to watch for in 2019. This report, based on their January 2019, covers the biggest 2019 healthcare trends, including the following:

• The business of healthcare including new market entrants, business models and shifting strategies to stay competitive.

• Increased consumer demand for more transparency

• Continuous quality and cost control monitoring across populations.

• CMS proposals to push ACOs into two-sided risk models.

• Fewer process measures but more quality outcomes scrutiny for providers.

Download

Downloadhis article is based on the January 2019 webinar “Healthcare Outlook for 2019” by Bobbi Brown, MBA, and Stephen Grossbart, PhD.

During the 2018 mid-term elections, candidates faced off with bold claims to fix the broken healthcare system. So what is the new congress doing to improve healthcare and fix the gridlocked political system? Beyond political maneuvering, 2018 saw material changes in the business of healthcare, including the increased pace of mergers and acquisitions as well as new measures from CMS to support transparency, interoperability, and a continued shift to value-based payments. These changes have significant ramifications for health systems in 2019 as the pace of change continues to increase.

Health systems constantly have to adapt to changes in their communities, populations, politics, and reimbursement structures. Understanding the current climate and the upcoming healthcare trends can help them stay abreast of important changes and be prepared for the future in order to stay financially viable. This article examines the impacts of the biggest changes to the healthcare landscape in 2018 and predicts 2019 healthcare trends that health systems should have on their radar.

Healthcare continues to be an important, but divisive political topic. Not surprisingly, 41 percent of eligible voters said healthcare was their key issue in the mid-term elections in 2018. In 2008, when the ACA became law, only 46 percent of voters supported single payer healthcare. That number has grown significantly to 59 percent approval in early 2018. While Medicare-for-all legislation is unlikely to pass both the House and Senate in its current form, there is a shift in public opinion with a solid majority now in favor.

Similarly, Medicaid is expanding. During the 2018 midterm elections, three states had ballot proposals to expand Medicaid, and two other states replaced governors who had blocked legislative attempts to expand Medicaid, resulting in a total of five new states that will expand Medicaid. Overall, the U.S. will likely increase Medicaid coverage to as many as 76 million enrollees by 2020.

Many states are also passing laws that make it easier for residents to access affordable healthcare. To that end, it seems Congress won’t repeal it–for now. Even with a Republican-majority House and Senate, there wasn’t enough support to repeal the ACA, so the ACA and the federal exchange should continue to thrive in 2019. Enrollment was down slightly in 2018 compared to 2017, but the numbers are still high. During the 2018 open enrollment period, 8.4 million people enrolled (down from 8.7 million in 2017).

However, while people are still signing up for insurance through the federal healthcare exchange, legal challenges to strike down the ACA still loom. A Texas judge ruled in 2018 that the entire healthcare law is unconstitutional because Congress had voted to remove the penalty for not having health insurance. According to the ruling, this effectively killed the constitutionality of the law because the Supreme Court had ruled that the original law (and penalty) was constitutional because Congress had the taxing authority to impose that fine. The judge’s 2018 ruling was quickly followed by legal analysts on both sides of the political aisle saying the judge’s reasoning was flawed, so it’s unlikely this ruling will stand. Regardless of the outcome, the ACA appears to be here to stay for the foreseeable future unless the Supreme Court steps in and makes changes.

While there’s partisan divide about the ACA, both parties agree on the importance of transparency. As Figure 1 illustrates, most states are not doing well in this arena. The maps provide transparency and quality scores for each state. Grey colored states on both maps indicate a failing grade, while blue states indicate an “A” for either quality or transparency.

Price transparency in healthcare is another big issue to watch for in 2019. Prior to January 1, 2019, California was the only state that required hospitals to post their prices online for consumers to view. As of January 1, 2019, CMS requires all hospitals to post prices online. However, prices don’t provide the whole story as patients’ costs remain a mystery. For example, if a patient has a hip replacement surgery at an outpatient center versus in a hospital as an inpatient his costs are going to vary considerably and include a wide range of variables. To aid consumers in understanding the billing process, Maryland state hosts a website where total cost is available for some procedures. The site shows the hospital costs and a potential total cost per condition, along with some quality metrics related to that condition for individual hospitals. This is a good example of how states can help improve transparency for consumers, enabling them to make informed choices about their healthcare.

Another healthcare initiative with strong political support is telehealth. That support likely comes from the fact that, according to HIT Consultant, Accenture conducted a 2018 survey showing that 78 percent of consumers are interested in receiving virtual health services. In 2019, Physician Fee Schedule regulation expanded coverage for telehealth and virtual care. Thirty-four states and the District of Columbia now require private insurers to cover telehealth the same way they would cover in-office services.

As healthcare grows and changes, new business models are taking shape. One of those models is personalization of healthcare services. Consumers are taking advantage of personalized healthcare options that provide a concierge model of service, accommodating the care they want at the time and location that’s convenient, such as the expansion of telehealth services. New models also means new market entrants and shifting strategies are driving changes in the healthcare landscape, with Amazon, Berkshire Hathaway, and JPMorgan’s foray into the healthcare space at the forefront. They’re not the only ones, however. Companies are seemingly entering the healthcare market from all directions and industries; Google is hiring physicians, including former executives of Geisinger Clinic and the Cleveland Clinic; Apple is investing in their Wellness Monitoring App; and even Uber is getting in on the action with the launch of Uber Health to help increase patient access.

Mergers and acquisitions are the norm with partnerships forming everywhere. For example, CVS is working with Aetna to combine 10,000 stores, 1100 clinics, and 22 million enrollees. The CEO of CVS, Larry Merlo, said about the move, “We are hard at work creating a plan to differentiate CVS Health in these patient journeys with the goal of making them simpler and more personalized while making care more actionable.” Cigna and Express Scripts combined to create insurer and pharmacy benefit company, and UnitedHealth Group’s OptumCare and other insurance companies are buying physician practices to try to control the first input into the healthcare system.

The list of partnerships and mergers of health systems seems endless. Meanwhile, many hospitals have closed their doors–a total of 21 in 2018 alone. While hospitals are closing, existing health systems are expanding their facilities. According to the American Hospital Association’s (AHA) 2019 Hospital Statistics report, 71 percent of respondents said their hospitals will be acquiring off-site outpatient locations. Looking at volume trends reported by the AHA, it’s clear that inpatient admissions are trending down, while outpatient care centers are increasing, which points to a change in the way healthcare is delivered.

According to National Research Council, the United States is among the lowest in terms of life expectancy out of 17 of countries with similarly high income. Health disparities take part of the blame. Variation in life expectancy across the county is dramatic. Access to healthcare services, education, early childhood development, and work conditions vary greatly. New York City is a perfect example of these disparities. In a presentation at the Institute for Healthcare Improvement in December 2018, Don Berwick stated that people who live on the upper east side of Manhattan have a life expectancy that is 10 years longer than those who live five miles north in the south Bronx. A breakdown of this shows that life expectancy declines by six months for every minute someone travels on the subway or 2.3 years for every mile driven.

Addressing these complex disparities is challenging, but some organizations are trying to do just that. For example, Rush University Medical Center in Chicago is taking ownership of the disparities. The organization’s stated goal is to work toward improving life expectancy, not only for students and employees, but for nearby communities as well. They are working towards this goal by hiring and developing local talent and increasing their minimum wage to roughly $22 per hour, which they believe is the minimum pay rate to support health. They also source and buy products locally rather than on a national level, and they’re investing in their communities with the goal of improving the quality of residents’ health and increasing life expectancy in the surrounding neighborhoods.

This visual below from the Democracy Collaborative provides more details about Rush’s aim to address healthcare disparities:

CMS is working to shift healthcare delivery from a fee-based system to a value-based system, which means the payment structure for Medicare payments continues to change. Most of the value-based programs CMS offers have been in place for several years and hospitals that participate are showing results in reduced readmissions. According to the MedPac report out in June of 2018, as the readmission rate declined, mortality rate and ED/observation rates were steady, but there was two billion dollars in annual savings, showing that the shift to value-based payments is making headway.

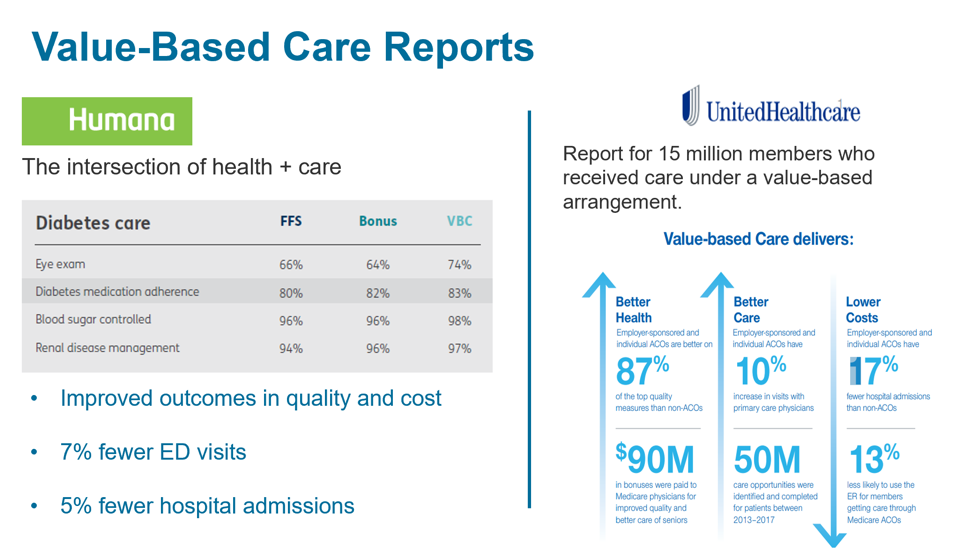

As predicted, the accountable care space grew in 2018 and will likely continue to grow. An ACOs goal is to take on real risk by adopting a true performance-based model that provides benefits if and ACO does well, but assesses fines if it doesn’t perform. This CMS model for ACOs, Pathways to Success, revolves around bundled payments and has five goals: accountability, competition, continued quality, integrity, and beneficiary engagement. This last goal is exciting. It means ACOs can talk directly to beneficiaries to offer incentives for care. United Healthcare has a value-based arrangement—a program it refers to as the intersection of health plus care.

United Healthcare reports that the 15 million members who received care under a value-based arrangement experienced improved health and better care at lower costs, illustrated in Figure 3 below.

Episodes of Care have taken healthcare organizations on a wild ride. These are bundled Medicare payments that started out as voluntary, then were mandatory, but are now again voluntary. The new voluntary episodes of care bundle, which began in October of 2018, is called Bundled Payments for Care Improvement (BPCI) Advanced. There are 1,547 physician organizations and hospitals signed up for BPCI, which includes quality scores as part of the program.

Some examples of bundling payments include major joint replacement, congestive heart failure, and sepsis. This program gives health systems an opportunity to get their feet wet, so to speak, and try out an episodes of care model before going all in.

With all of these changes afoot, there are several keys for health systems to stay ahead of the game in 2019. Health systems should have a clear understanding of their goals and develop a strategic plan based on current knowledge of the healthcare landscape. When it comes to ACOs, bundles, and risk-based contracts, health system leaders should be ready for a growing data burden and make sure there are analysts on board who know how to analyze claims data. Building capacity to integrate claims and clinical data is also critical. Another trend that’s worthy of following is collaboration with community partners to improve healthcare delivery and reduce disparities.

Health systems must be agile enough to adapt to changes in the industry including new healthcare business models, mergers and acquisitions, and reimbursement structures. Understanding this landscape and the new expectations can help keep them viable for the future of healthcare.

A poll of a 2019 Healthcare Trends webinar attendees showed that nearly half of attendees believe that consolidation and changing business models will be the top healthcare story in 2019, with big market share gains in new care delivery models and consumerism coming in second and third, respectively. No matter what happens in 2019 and beyond, one thing is certain: healthcare organizations will have to change and adapt in order to meet the challenges of the evolving healthcare landscape.

Would you like to learn more about this topic? Here are some articles we suggest: