I am one of the brave souls who takes the time to read the report issued each spring by the Medicare Payment Advisory Commission (Medpac).

The report shows the numbers of Medicare beneficiaries and claims are growing; healthcare organizations are increasingly losing money on Medicare; payment increases certainly will not keep pace with declining margins; and Medicare policies will continue to incentivize quality and push providers to assume more risk.

But the report also reveals that some healthcare organizations—referred to as “relatively efficient”—are making money from Medicare with an average 2 percent margin. How do you become one of these organizations? And how do you target and counter Medicare trends that impact your business?

Download

Download

Editor’s Note: Originally written July 9, 2013, Bobbi has updated this piece for March 2018.

Given the continued trends for declining Medicare reimbursements, I am one of the brave souls who takes the time to read the report issued each spring by the Medicare Payment Advisory Commission (Medpac). MedPAC is a nonpartisan agency that provides Congress with analysis about the Medicare program. Many of their reports are used to set policy for the Medicare program. The push for quality is strong and MedPAC is working to provide the right incentives for quality.

Though the reading can be a bit dry, the information contained in the report is important—particularly considering the fact that the commission’s recommendations are influential in shaping policy. Medicare payment policies tend to set a precedent for other payers.

I had the chance to read a variety of the documents published by MedPAC (Medicare Payment Advisory Commission). I reviewed two documents:

The Report to Congress covers 10 areas from stand-alone ED to provider payment. I am just focusing on a couple of the areas and showing a few key findings from the data distributed.

The reports show the spending trends are not affordable long-term. We have been able to lower the per beneficiary spend but we need to sustain that trend

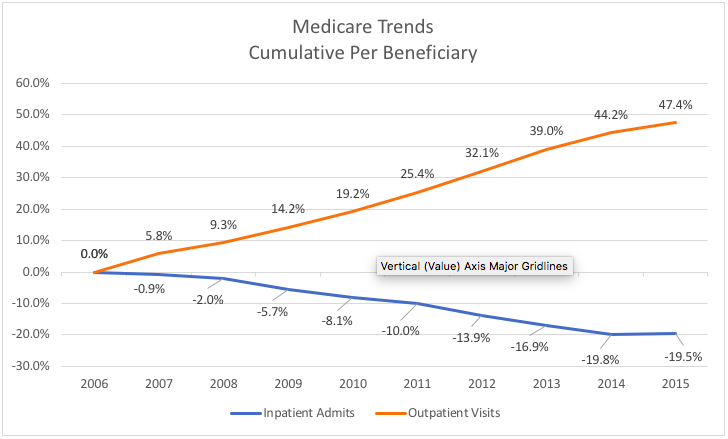

From 2006 to 2015 in the Medicare program, outpatient visits per beneficiary increased 47 percent and inpatient admissions declined by almost 20 percent. See the chart below illustrating this shift in services.

During the same time, Medicare length of stay decreased 7.7 percent. These facts will impact the location of services for the populations served.

Source: MedPAC analysis of CMS claims

There have been a couple of shifts in the type of cases admitted to the hospital between 2006 and 2015.

The outpatient shift will continue, and we need to plan for facilities and consumer preference.

In 2013, the Hospital Readmission Reduction Program (HRRP) started calculating penalties for hospitals that have above-average readmission rates for selected conditions. From 2010 to 2015 the potentially preventable readmission rates declined from 12.9 percent to 10.5 percent for all conditions. The three conditions covered under the HRRP beginning in 2013 have experienced declines in potentially preventable readmission rates. Readmissions for AMI declined 3.6 percentage points, heart failure declined 3.1 percentage points and pneumonia declined 2.5 percentage points.

CMS started a program that involves a negative payment and hospitals have responded to the penalty by working to lower readmissions.

In 2015, about 46 percent of all Medicare fee-for-service patients were discharged from an acute care hospital to home, without any organized post-acute care. This represents a decrease 7 percentage points from 2006. More Medicare patients are being discharged to post-acute care services. Twenty-one percent are discharge to skilled nursing care and seventeen percentage are going home with organized home-health care services. MedPAC is recommending implementation of a unified payment system for post-acute care. Medicare currently has seen differences for similar patients based on the post-acute venue chosen. The supply and use of post-acute providers varies considerably across the country. MedPAC would like payments based on patient characteristics rather than site of service.

Bundle payments would help in this area and place accountability with the organization that assumes the risk. Also CMS may revamp the payment system for post-acute care by 2020.

The costliest 25 percent of beneficiaries account for 84 percent of the spend. The costliest areas of spend include dual eligible (Medicare, Medicaid recipients), beneficiaries with multiple chronic conditions, users of inpatient services and those in last year of life.

CMS needs to develop programs that target and value care coordination.

MedPac devoted several charts to display low-value care. The definition of low-value care is the provision of a service that has little or no clinical benefit. They used a set of 31 measures developed by a team of researchers. Then they applied dollars to the list, and the spend for 2014 was $2.4 to $6.5 billion. The list includes testing, imaging and screening. Some high spend examples are stress testing for stable coronary disease and imaging for nonspecific low back pain. They stated this is just a start to determining the cost of low-value care.

Providers should be evaluating the 31 measures in their institutions. We may currently get revenue for the services, but we need to shift to a value lens.

I am hoping you can see from these facts that those recommending new policies will continue to push providers for quality and value. More beneficiaries are entering the program and there will be constant pressure to control the cost. There is a willingness to pay for better outcomes. Using data to derive insightful analytics through platforms such as the Health Catalyst® Data Operating System (DOS™), healthcare organizations can approach these changes with confidence that they can adapt and thrive in a more value-based environment.

Would you like to use or share these concepts? Download this presentation highlighting the key main points.

Click Here to Download the Slides

https://www.slideshare.net/slideshow/embed_code/key/IdigRUwovnv54Q